By: Geeq on Jun 27, 2019

Facebook Announces The Libra Coin

In the past week, Facebook announced its plans to launch a digital currency called Libra. According to Bloomberg, Libra will be “supported by established government-backed currencies and securities” where the “goal is to avoid massive fluctuations in value so Libra can be used for everyday transactions across Facebook in a way that more volatile cryptocurrencies, like Bitcoin, haven’t been.”

The news of this exciting new international cryptocurrency with strong connections to well-established financial institutions was echoed across the internet. TechCrunch reported “The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen.”

TechCrunch went on to say: “The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.”

The basic message was that Libra was going to be something like a stable-coin, only better and safer. This was a description that was widely echoed on crypto and financial news sites and forums.

Why Not a Stable-Coin?

Stable-coins are problematic, in general. The one and only way to support a fixed valuation for a stable-coin is to maintain a 100% reserve of the backing currency or commodity in question. (The fundamental problems and challenges associated with stable-coins are discussed in an accompanying piece here.)

In addition, stable-coins necessarily require trust in the institutions that back them, as well as in the integrity and cooperation of the banks and regulatory authorities that enable it.

Libra promises it will be fully collateralized, which appears to address the first issue but, as we describe below, serious concerns remain.

Exchange Rate Variation

In contrast to the public’s perception of the Libra as a carefully conceived and safe medium of exchange, The Libra Association has gone on record to say Libra is not exactly a stable-coin. Rather, it will be “a blend of multiple currencies,” so its value “will fluctuate in any given local currency, and exchanges will charge a spread above or below the value of the reserve.”

However, the decision to use a basket of currencies creates a new set of problems that stem from exchange rate variations. As a result, it is highly unlikely that Libra will meet users’ expectations as the globally ubiquitous payments network that many suspect it aspires to become. (Paypal, Mastercard, and Visa have all joined The Libra Association.)

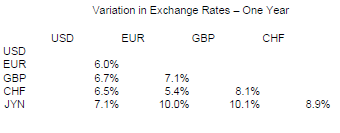

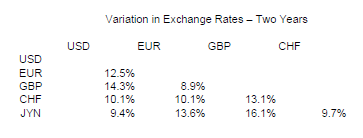

The tables below show the percentage variations in exchange rates over the most recent year and two years, respectively.

As you can see, exchange rates between each pair of currencies experienced fluctuations between 6–10% from June 25, 2018-June 25, 2019 and 9–16% from June 25, 2017-June 25, 2019.

One might think that choosing a basket of currencies would reduce volatility just like diversifying a stock portfolio. Ironically, it actually increases the volatility from the standpoint of an individual consumer. Consider the following simple example.

Suppose half of Libra’s reserve is in USD and the other half in Euros, and the USD loses 6% of its value compared to the Euro. Anyone who bought a Libra for Euros and then cashed out (in Euros) would receive 3% less than he put in, since the value of the basket as a whole has gone down relative to the Euro. On the other hand, anyone doing the same in USD would get 3% more.

Holding a Libra, in this example, is like changing half the cash in your pocket into Euros and half into dollars. This might be nice if you happen to pay your rent in dollars, but if you pay your rent in Euros, then you will find the value of your Calibra wallet has shrunk by 3%.

In fact, the relationship between local currencies and local prices is one of the reasons most people only hold the currency they normally buy and sell with. Even when the value of the local currency drops on international markets, its local purchasing power is largely unaffected.

Before you ask, re-balancing the basket does not help. The reasons are complicated, but to get a sense of them, consider again the example above.

The example showed if we simply held a fixed ratio of currencies, we have a zero-sum game. Libra holders who use Euros lost exactly as much as holders who use dollars gained.

If re-balancing the currencies in the basket over time happens to shift this ratio in favor of currencies whose values increase, all would gain, while all would lose if the ratio shifted toward currencies whose relative values decrease.

Therefore, the only way for Libra holders to win, on average, is for The Libra Association to systematically outguess the market.

In other words, winning has nothing to do with some magical mathematical portfolio diversification formula. It depends entirely on being lucky in the broader zero sum game of international currency exchange markets.

The Inflation Tax and Interest Rates

Recall inflation is like a tax on holding cash or cash equivalents. For example, if the US had a 5% inflation rate over a year, an apple that cost you $1 at the first of the year would cost you $1.05 at the end of the year. Put another way, it would be as if each dollar bill in your wallet magically turned into $0.95 in change over the course of the year.

Interest rates compensate lenders for delaying consumption. For example, I might be willing to give you a chocolate bar today if you promise to give me two chocolate bars next week — for an implicit interest rate of 100% per week.

What would happen if we knew that next week, government policy would cut the size of each chocolate bar by one-third? If I was only willing to give up a regular sized chocolate bar today for the equivalent of two regular sized chocolate bars next week, you would have to offer me three new, smaller sized chocolate bars (after inflation) as a promise to repay me, for me still to be willing to lend you my chocolate bar today. If you took that deal, I would get my implicit real interest rate of 100% in ounces of chocolate, but in monetary units (since the chocolate bar is standing in for a dollar), the nominal interest rate has increased from 100% to 200%.

In the same way, interest rates on government and corporate bonds are set by the market and are directly affected by inflation. If the inflation rate is 5% and investors demand a 2.5% real rate of return, then the nominal interest rate must be approximately 7.5%. With inflation, each individual new dollar a lender receives in the future is worth less, but with an appropriate adjustment in the interest rate, that same lender can buy 2.5% more by making the loan.

Funding The Libra Association

The Libra Association’s current plan is to put the cash it collects from selling Libras into interest bearing accounts and bonds, some of which will be short-term securities from central banks. CNBC states, “Money for the reserve will come from people who use Libra and Libra Investment Tokens that are bought by founding members of the nonprofit association.”

The Libra White Paper elaborates:

Interest on the reserve assets will be used to cover the costs of the system, ensure low transaction fees, pay dividends to investors who provided capital to jump start the ecosystem (read “The Libra Association” here), and support further growth and adoption. The rules for allocating interest on the reserve will be set in advance and will be overseen by the Libra Association. Users of Libra do not receive a return from the reserve.

Buying Libra is the same as lending money to The Libra Association at a zero interest rate. As the last sentence of the policy stated, a user of Libra does not receive a return. In other words, a consumer who purchases a Libra today is only promised the future value of a Libra when she cashes out.

On the other hand, if and when The Libra Association accepts currency for its Libra Coins, it plans to invest that money by making loans to central banks or corporations. As a lender, The Libra Association will reap the benefits of the interest it earns. Since a nominal interest rate includes the inflation rate, the more inflation, the more the Libra Association earns on its basket of reserve holdings.

Inflation rates over the last few years, for the currencies proposed for the Libra basket, have generally been between 1–3%. That is not a bad return in itself, but these rates are quite low in a broader historical context. The US government is borrowing more than one trillion dollars per year, Brexit and trade wars may cause recessions in Europe at some point, and the demographics in many countries will probably result in increased spending just as tax revenues from labor income decrease.

All these trends will tend to make capital more scarce, demand for borrowing higher, and increase the likelihood that governments will print money to keep up with interest payments, driving up inflation rates.

What all of this suggests is that the inflation taxes, which typically go to the governments that print their currencies, will now go to Facebook and The Libra Association instead. Libra users still will pay the inflation taxes but, by and large, will not be eligible for dividends or returns from reserves. If users were to put their dollars or Euros into their bank accounts, they would get interest payments that would have done more to keep their purchasing power constant than owning Libras.

In addition, Libra users are exposed to the inflation rates of other countries, which they would not have been, had they continued to purchase goods and services from vendors with their cash in their own country’s currency.

If Libra really does become as significant a player in the payments space as The Libra Association hopes, it possibly would become a destabilizing force on the international monetary system. Suppose the Royal Bank started to print pounds at a high rate, resulting in significant inflation. The Libra Association may decide to reduce its GBP holdings dramatically. Dumping the pound could lead to further decreases in its exchange rates compared to other currencies. While this may not be as much of a concern for the dollar or the Euro, for smaller currencies like the Swiss Franc, even the threat of such an exit could be used as a political tool to pressure governments.

Conclusion

While the monetary policy proposed for the Libra sounds like an innovative way to protect users from the vagaries of cryptocurrencies, a more careful analysis shows it is quite the opposite. The use of a basket of currencies to collateralize the Libra’s value exposes account holders to significant new risks, generated by exchange rate variations and inflation in other countries. The Libra Association will benefit from inflation at the expense of governments and account holders.

Users can easily avoid all of these problems by simply using cash or checking accounts. In sum, Libra is a step backwards for consumers. Although it may not be immediately evident, the proposed system introduces a downside for consumers when significant inflation leads to an increase in exchange rate volatility for fiat currencies. In the unlikely event that Libra gains widespread adoption, there is the potential for Facebook and The Libra Association to be able to influence governments and the stability of the international monetary system.

Our Work

Geeq is a start-up permissionless blockchain infrastructure-as-a-service company. Geeq has developed an innovative monetary policy for a stabilized-token, rather than a stable-coin. As a result, Geeq will not have the problems associated with stable-coins or any of their variants. For the interested reader, Geeq’s monetary policy is published at Geeq.io.

To learn more about Geeq, follow us and join the conversation.

@GeeqOfficial